{kind=link}

Most investors will never read far enough to find this, but Zepto openly discloses it does not meet SEBI's standard eligibility criteria for a public listing. The normal route requires a company to have maintained a certain level of operating profit and net worth over three consecutive years. Zepto has neither.

It is listing through a special regulatory provision designed for companies still in growth mode that have not yet crossed the profitability threshold. The practical consequence is structural: at least 75% of the shares on offer must go to institutional investors, and retail investors get no more than 10% of the allocation.

This is not buried. It is disclosed. But it sits deep inside the risk factors, which means the people with the smallest allocation are also the least likely to know why their allocation is small.

The Profitability Numbers, Side by Side

Zepto's preferred headline metric is Adjusted EBITDA per Order. The harder number, Free Cash Flow per Order, tells a slightly different story. Both are in the filing. Neither is positive.

| Metric | FY2024 | FY2025 | FY2026 |

|---|---|---|---|

| Adjusted EBITDA per Order (₹) | (84.64) | (136.15) | (78.75) |

| Free Cash Flow per Order (₹) | (93.43) | (160.56) | (67.63) |

| Free Cash Flow, Total (₹ Mn) | (12,413.83) | (53,324.89) | (43,295.42) |

| Net Cash Used in Operations (₹ Mn) | (10,978.80) | (46,248.34) | (34,624.42) |

Source: DRHP peer benchmarking table and summary financial information

The direction of travel is genuine. Free Cash Flow per Order improved from ₹(93.43) in FY2024 to ₹(67.63) in FY2026, and the most recent quarter came in at ₹(42.01). Every order still costs more cash than it earns, but the gap is narrowing consistently.

The reason this matters: Zepto's investor narrative centres on the "path to profitability." The filing is honest that the destination has not been reached. What it is less emphatic about is that Adjusted EBITDA involves several add-backs that make the number look better than the raw cash position. Free Cash Flow per Order is the harder, cleaner measure and it gets far less airtime.

Zepto Is Quietly Becoming an Advertising Business

This is the most strategically significant shift in the entire filing, and it is almost entirely absent from mainstream coverage.

Zepto has made a conscious decision to keep its retail margins deliberately low, not to maximise them. The logic: lower prices and platform fees keep users ordering more frequently and keep merchant partners on the platform. The margin it foregoes on groceries, it recovers by charging brands to advertise. The filing explicitly states that Zepto uses advertising revenue to offset any reduction in platform commissions from merchant partners.

The numbers show how fast this has moved:

| Advertisement Revenue | FY2024 | FY2025 | FY2026 |

|---|---|---|---|

| Revenue (₹ Mn) | 491.72 | 6,512.41 | 16,357.26 |

| Year-on-Year Growth | — | 1,224% | 151% |

Source: DRHP MD&A section

In three years, advertising went from a rounding error to the company's most interesting growth lever. Zepto is increasingly a performance marketing platform for FMCG and consumer brands, with a delivery network attached. The dark stores are, in a sense, fulfilment infrastructure for a media business. This model has real precedent. It is broadly how Zomato and Amazon India built sustainable margins. But it introduces a dependency on brand advertising budgets that pure grocery retail does not have. If advertiser spending on quick commerce softens, or brands start demanding better ROI attribution, this revenue line becomes vulnerable in a way the filing does not fully stress-test.

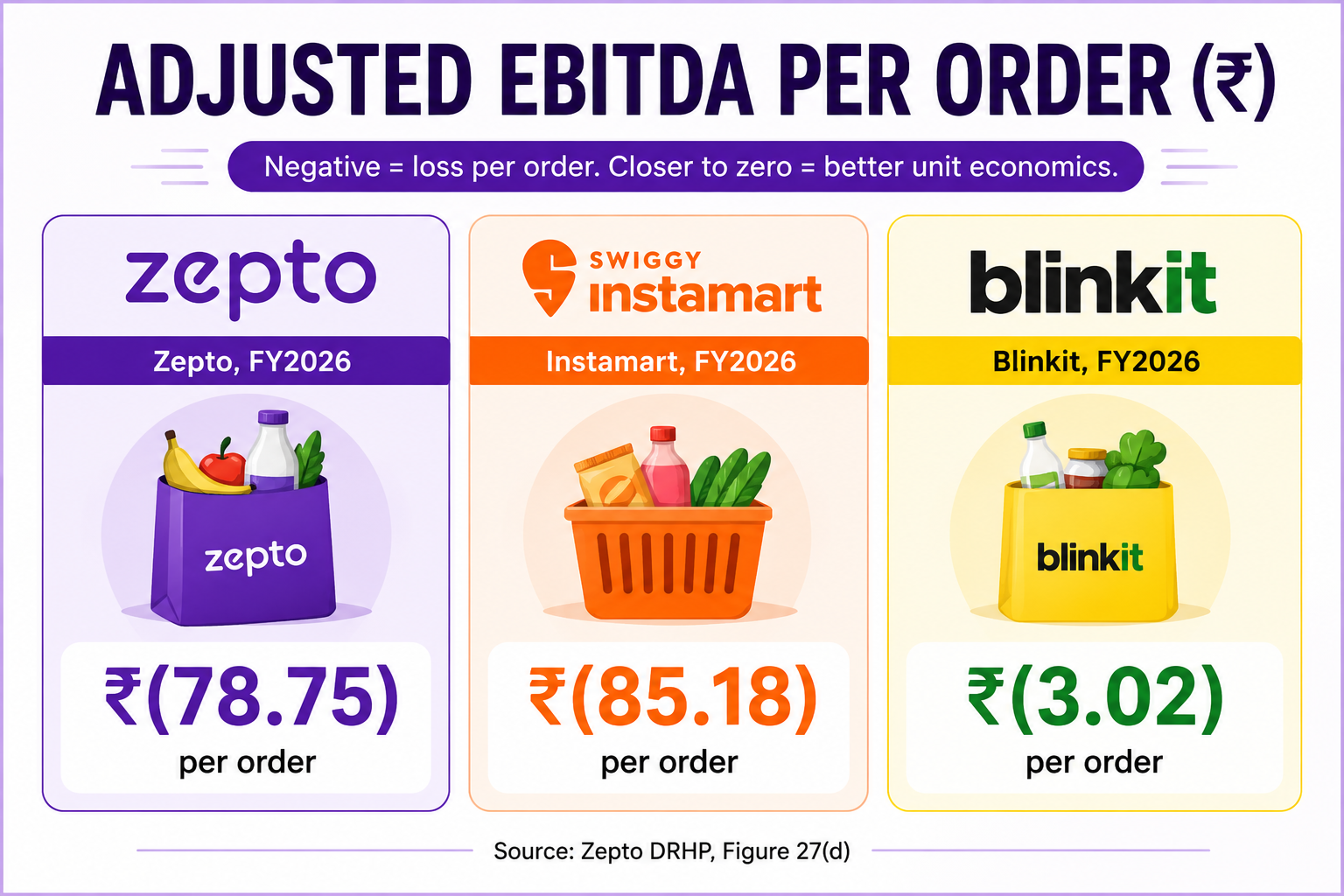

The Peer Comparison That Asks the Biggest Question

The filing compares Zepto against its two main rivals, Instamart and Blinkit, on Adjusted EBITDA per Order. This is the one profitability metric available for all three since Swiggy and Zomato are listed companies.

| Adjusted EBITDA per Order (₹) | FY2024 | FY2025 | FY2026 |

|---|---|---|---|

| Zepto | (84.64) | (136.15) | (78.75) |

| Instamart | (74.60) | (73.35) | (85.18) |

| Blinkit | (18.92) | (6.89) | (3.02) |

Source: DRHP Figure 27(d). Note: Blinkit and Instamart figures are sourced from Zomato and Swiggy's public segment disclosures as interpreted by Zepto, not independently audited standalone figures.

Blinkit's Adjusted EBITDA per Order in FY2026 was ₹3.02. Zepto's was ₹78.75. Two businesses, same market, same product, targeting the same customer. The filing presents this data without commenting on the divergence. Investors are left to decide whether Zepto’s path to Blinkit-like unit economics is a matter of time and scale, or whether there are structural differences in how the two businesses operate. The filing offers no clear answer either way.

The ED Summons Nobody Was Expecting

This is the disclosure that emerged today and is the most significant new development in the updated filing.

Both co-founders, Aadit Palichaand Kaivalya Vohra, received summons from the Enforcement Directorate on April 8, 2026, under the Foreign Exchange Management Act. The ED sought a wide range of documents: details of foreign and overseas investments, audited balance sheets since FY2021, shareholding patterns, loans and guarantees, income tax returns, bank accounts, immovable properties, and a note explaining the company’s business model.

Vohra appeared before the ED on April 17 and April 22. Palicha appeared on April 20 and May 15. Both provided documents and information requested, including follow-on details on the holding structure, the re-domiciling scheme, and business agreements. As of the filing date, no further communication has been received from the ED.

Two things stand out. First, the company disclosed this in the Risk Factors section, not the standard outstanding litigation section, which signals it considers this material for investors assessing the IPO. Second, the summons arrived just weeks before the updated DRHP was filed. A FEMA summons is not itself a violation or finding. Regulators routinely seek information to establish whether any contravention occurred. But for a company about to ask the public for ₹10,000 crore, the timing and the breadth of information sought, going back to FY2021 and covering the entire overseas holding structure, deserves careful reading.

Three More Regulatory Disclosures in the Same Filing

The ED summons is not the only regulatory matter in the filing. Three others sit nearby and are receiving considerably less attention.

The Competition Commission of India has an active inquiry into predatory pricing and anti-competitive discounting in quick commerce, in which Zepto has been named alongside other quick commerce platforms. Separately, the All India Consumer Products Distributors Federation has written to SEBI seeking to block quick commerce IPOs entirely, citing deep discounting and cash-burn-led market capture.

The third: the Central Consumer Protection Authority previously issued notices to Zepto for alleged use of dark patterns on its platform, specifically “Misleading Advertisement,” “Basket Sneaking,” and “Drip Pricing.” CCPA directed the company to pay a penalty of ₹0.70 million and take remedial action. Zepto has appealed before the National Consumer Disputes Redressal Commission. An interim stay was granted on January 20, 2026. The matter is currently pending.

Individually, none of these is a company-defining risk. Together, they paint a picture of a business operating under meaningful regulatory scrutiny across consumer protection, competition law, and foreign exchange management, all simultaneously, all ahead of an IPO.

The Food Safety Picture Is Larger Than One Story

The filing discloses more food safety proceedings than most coverage has noted. The Ghaziabad cases, two notices over a packet of jaggery and a packet of puffed fox nut, are the most visible. The food safety officer subsequently filed two suits before a local magistrate's court, naming the company and one of its managers, and those suits remain live.

But the litigation section reveals a wider pattern. The Maharashtra Food and Drug Administration has filed multiple adjudication proceedings against Zepto across several Mumbai establishments, covering allegations including operating without a valid food business licence, substandard food samples, expired products being found on premises, and holding duplicate FSSAI licences. One of these proceedings names co-founder Kaivalya Vohra as the nominee of the company. These cases are all from 2025 and 2026. They are not legacy issues from a pre-IPO cleanup. All are currently pending.

None of these individually threatens the business. But Zepto operated 1,139 dark stores across 66 cities as of March 2026 and plans to expand to approximately 1,904 stores using IPO proceeds. Each store handles perishable and packaged food. The compliance surface area is large, growing fast, and does not appear in any financial projection.

The Auditor Change That Offers No Explanation

In March 2024, Zepto's previous audit firm, Ruthala & Co., resigned. The reason stated in the filing: “preoccupation.” A new auditor from the EY network, S.R. Batliboi & Associates LLP, was appointed two days later and has since conducted the audits presented in this DRHP.

The disclosure is complete by regulatory standards. No further explanation is offered anywhere in 690 pages. Auditor transitions ahead of IPOs are not uncommon, and the new firm’s work underpins the financial statements investors are relying on. Whether the departure was entirely routine is simply not something the document helps you assess.

The ESOP Overhang Above the IPO

The filing discloses over 1.2 billion stock options currently outstanding, with an exercise price of ₹0 for all of them. If fully exercised, these would result in roughly 928 million additional equity shares entering the market at no cost to the holder.

This is standard for a company at this stage, and ESOPs are a legitimate and necessary tool for retaining talent in a competitive market. But retail investors buying into the IPO are absorbing this dilution overhang. The fully diluted EPS for FY2025 was ₹(5.05), already reflecting this, which is worth keeping in mind when evaluating any per-share metric.

Where the Business Actually Stands

The filing's own numbers, read together, make the picture clear:

| Metric | FY2024 | FY2025 | FY2026 |

|---|---|---|---|

| Revenue from Operations (₹ Mn) | 44,545.16 | 1,11,099.47 | 2,26,235.84 |

| Restated Loss for the Year (₹ Mn) | (12,147.94) | (46,997.14) | (59,051.92) |

| Closing Cash incl. Investments (₹ Mn) | 16,882.61 | 74,407.72 | 56,805.27 |

| Net Cash Used in Operations (₹ Mn) | (10,978.80) | (46,248.34) | (34,624.42) |

| Orders Per Day | 3,63,033 | 9,09,881 | 17,53,915 |

| Return on Net Worth | (13.69)% | (29.80)% | (43.23)% |

Source: DRHP summary financial information and key operating metrics

Revenue has roughly doubled each year. Losses have grown in absolute terms, though there are genuine improvements in per-order efficiency. The cash balance of ₹56,805 million against operating cash consumption of ₹34,624 million gives roughly 1.6 years of runway at current burn, before IPO proceeds arrive. Return on Net Worth has been negative in every reported quarter.

Zepto is not raising money because the business is generating returns. It is raising money to continue building the business it believes will eventually generate returns. That is a legitimate investment thesis, and the growth metrics, 4.79 crore annual transacting users, 2.33 million orders per day in Q4 FY26, orders per store rising from 1,425 to 2,140 in a single year, show the underlying business is genuinely scaling.

What the filing is asking investors to do is price in a future that has not yet arrived, while being transparent about the regulatory, operational, and financial uncertainties that stand between now and then. The disclosures are all there. Whether investors read them is another matter entirely.

Original Article

(Disclaimer – This post is auto-fetched from publicly available RSS feeds. Original source: Startuptalky. All rights belong to the respective publisher.)